When is a “Connectors” Business a Good Business Model?

There has been an explosion of companies following a “Plaid for X” business model focused on moving data across an industry. This is an overview of what I believe makes some connector businesses successful, and others unsuccessful.

Travis May

Chief Executive Officer

·

12 min

Background on the Explosion of the Connectors Space

A decade ago, very few startups were in the business of building data connectors; MuleSoft was seen as a contrarian with a small TAM for building in the space, and the other middleware players (eg. TIBCO) were all considered “legacy” businesses. That has changed recently: just this week, the largest data connector deal ever was announced, and there has been an explosion in both horizontal connector businesses (ranging from Zapier to Airbyte) as well as connector businesses in every vertical (from Redox in healthcare to Catena in telematics to Segment in marketing). This explosion of the connector space is due to three factors:

The increase in the value of data

The explosion in the number of places where data resides

The explosion in the number of applications that exist that use data

Failure Scenarios of Connector Businesses

Several of these businesses are currently “hot,” but there are many more failed “Plaid for X” models than there are successes.

Most connector businesses fail, likely due to:

They can’t get the most valuable integrations

An industry doesn’t actually need lots of integrations

“Connectors” become a mask for low-margin services rather than repeatable technology

The company builds lots of integrations with cool technology, but so do 5 other connector businesses — so they fight relentlessly on price

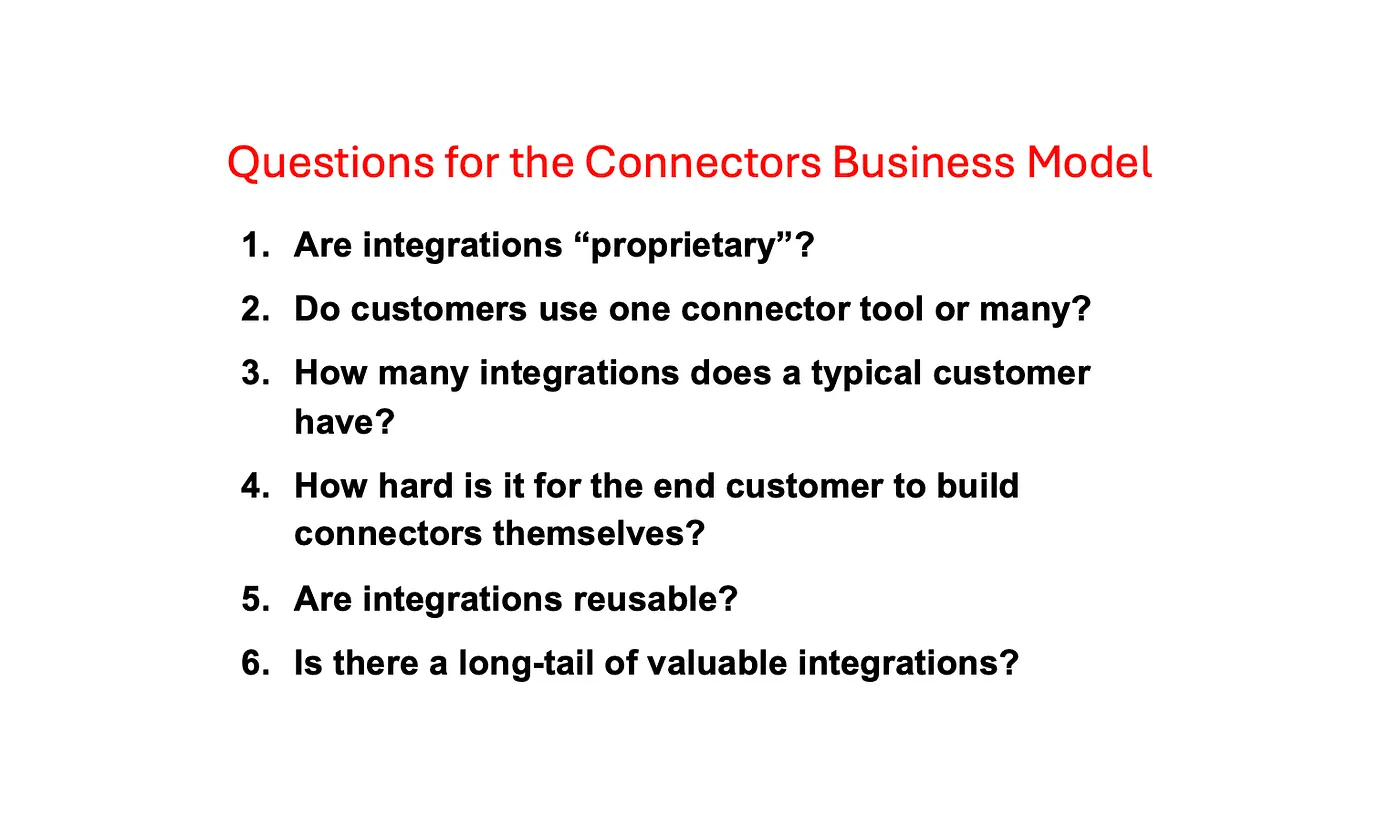

The 6 Questions for Successful Connector Businesses

Against this backdrop, I have landed on six questions I ask about a “connector” strategy.

Press enter or click to view image in full size

Are integrations “proprietary”? For a connectors business to be long-term viable, it needs some of its connectors to be defensible via “proprietary” integrations. This takes two forms as connector businesses get big: 1) some data sources that don’t have an “open API” allow you to establish a proprietary integration (e.g., Plaid’s integrations with banks), and/or 2) companies integrate into you (e.g., Okta’s integrations with applications). While you may start with “open APIs”, you cannot build defensibility on these alone; as you get scale you ideally take advantage of that scale to break into proprietary integrations. At LiveRamp, for example, we focused on integrating with every media platform; at the time, about half had a standard integration template, but about half would only prioritize integrations if a client pushed for them. This created a network effect in the business as winning clients helped us win more integrations.

Do customers use one connector tool or many? “Connector Gravity” is important for long-term defensibility; if customers decide integration-by-integration which connector tool to use, you have much less defensibility and stickiness. For Datavant and LiveRamp, customers needed a common ID, so it made sense to use one source of integrations and there was a high level of gravity; similarly, SSO from Okta has a high level of gravity because of the user experience. But many other integrations businesses have low gravity and are forced to compete connector by connector.

How many integrations does a typical customer have? The more integrations a customer has, the better. If it’s only a handful, it’s hard to have a large business. Most enterprises use thousands of vendors that hold or need data, though, so many spaces have room for lots of integrations.

How hard is it for the end customer to build connectors themselves? The upper bound of value a connectors business creates is the cost for an end customer to build an integration in house. The more complex an integration is, the better. In both the Datavant and LiveRamp businesses — the first integration was very difficult to build, the next 20, somewhat difficult, then increasingly easier, until integration 100 was almost automatic as we relentlessly templatized. This made the “build vs. buy” calculus very clear; it made no sense for a customer to build something in house.

Are integrations reusable? The economics of a connectors business work best if you can amortize an integration across many clients by building the integration once, then reusing it across clients. This varies based on the industry and type of integration.

Is there a long-tail of valuable integrations? In some industries, the dominant player has so much market share that connectors are less valuable. For example, there are parts of healthcare where Epic has so much market share, that integrating with the “long-tail” doesn’t create enough value. The more fragmented the industry, the better it is for connector businesses.

As data gets used more and more for AI applications, I expect more and more niche connector businesses will emerge. In most cases, these won’t succeed — as they won’t meet the criteria above and they’ll end up being commoditized away. But I expect at least a dozen more connector unicorns will be formed this decade when entrepreneurs are thoughtful about these questions.

Disclosures: I am a shareholder, board member, and advisor to many “connector” businesses.

Travis May

Chief Executive Officer

Travis May is the Founder and CEO of Shaper Capital, a company dedicated to building businesses that solve data fragmentation across industries.

Travis has a proven track record as a serial entrepreneur, having previously led the two biggest data exits of the last 20 years as co-founder and CEO of both LiveRamp and Datavant. LiveRamp, which pioneered data onboarding, is now a publicly traded company (NYSE:RAMP); he scaled it to over $200 mm in revenue. Travis then founded Datavant, which became the leading platform for healthcare data interoperability. Under his leadership, Datavant merged with Ciox Health in a $7 billion transaction, creating the largest health data ecosystem in the United States.

Travis graduated with magna cum laude and phi beta kappa honors from Harvard University with degrees in economics and mathematics. He has been recognized by Forbes’ “30 Under 30” list and AdAge’s “40 Under 40” for his impact in technology and business. Travis lives in North Carolina with his family and is focused on building the next generation of world-changing companies.

By clicking “Accept All Cookies”, you agree to the storing of cookies on your device, including to enhance site navigation and analyze site usage. More info

By clicking “Accept All Cookies”, you agree to the storing of cookies on your device, including to enhance site navigation and analyze site usage. More info

.png)